Mobile virtual cards can be a catalyst for digital transformation by issuers

Commercial cards has spent the last few years digitising its business, but digital transformation is now required to open up to new business models and revenue opportunities.

There are countless articles and seminars on how virtual cards are helping business customers of banks to automate and digitalise their own payment processes. However there is much less spoken about how they will also enable (or perhaps force) commercial card issuers into their own digital transformation, in particular within their customer channels.

Virtual cards are an exemplar of payments digitalisation, defined as digital technologies that change business models, creating new revenues and value producing opportunities. And it is tokenisation that is the technology that raises virtual cards above being simply a digitised representation of the plastic card in a mobile wallet.

Interestingly the resultant use cases have been very different in the consumer card space versus B2B, and this has created some market confusion in the terminology around virtual cards.

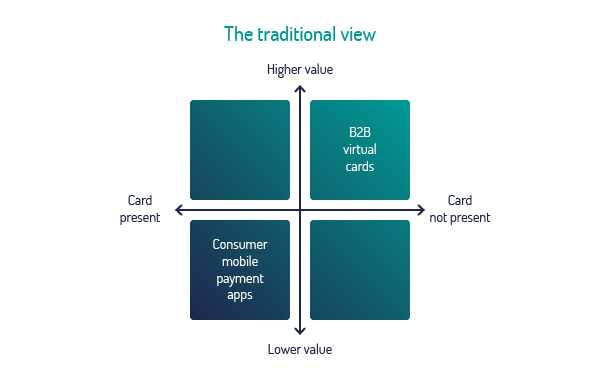

To those of us from a commercial cards background, virtual cards are typically limited use tokens that have found extensive use in the 2010’s particularly for invoiced payables in North America, and within the travel intermediary vertical. They have been largely used for higher value, card-not-present use cases.

For those with a consumer cards background, virtual cards may relate to mobile payment apps, whether these are simply digital representations of plastic cards or tokenised payment instruments, their initial use cases have been predominantly based on lower value, card-present transactions.

The differences are also noticeable in distribution – B2B virtual cards being made available through APIs, web portals and batched files, whereas consumer virtual cards are typically deployed in a digital wallet on a smartphone.

Today those traditional boundaries are blurring and convergence of these two models will characterise virtual cards in the 2020’s. Increasingly consumer mobile payment applications like Apple Pay are moving into the online, eCommerce space, and B2B virtual cards will find their way into payment apps and wallets, which in turn will open up a range of new use cases for commercial cards. Ultimately all this change signals the beginning of the end of plastic.

And this is where the rubber meets the road as far as commercial card issuers are concerned. In the same way that virtual cards are more than just a new form factor, banks need to also look more closely at their customer channels. Are they really fit for purpose to support digital payments – in particular requesting, provisioning and using mobile virtual cards?

Digitisation is the conversion of analogue to digital, and for most banks their commercial card apps and portals have been built with the primary objective to remove paper processes and calls from the call centre. The customer tooling has been principally focused on post-purchase information such as transactional data, balances, statement information and possibly expense management capabilities.. This has clearly driven cost savings for the issuer, but let’s be frank, their general lack of use by cardholders/ employees and Programme Administrators is probably indicative that they have not been critical to the customer journey until now. But that will not be good enough in a new world of mobile virtual payments.

Some early adopters of mobile virtual cards in the B2B space have launched them through a separate portal/ mobile app, but in truth the last thing a business traveller really wants is another disconnected app to navigate in their business travel customer journey.

We talk about the consumerisation of commercial payments, and that will require greater connectedness and engagement with businesses throughout their customer journey. Mobile virtual cards bring a new dimension that potentially requires the re-design of these channels, so that they can address needs pre-, in- and post-purchase. Commercial cards are being digitalised, and the channels through which they can be instantly requested, provisioned and utilised must similarly reflect that customer need.

Digitisation and digitalisation are two words that are often used interchangeably in business, when in fact they are really quite different. Commercial cards has spent the last few years digitising its business, but digital transformation is now required to open up to new business models and revenue opportunities, and mobile virtual cards are undoubtedly helping to be a catalyst for that change.