SME spending pushes commercial cards volume closer to pre-pandemic levels

Card payments giant American Express recorded a sizable 44% growth year on year in the commercial payments business from Q2 2020 while Visa saw a decline of 4.7%.

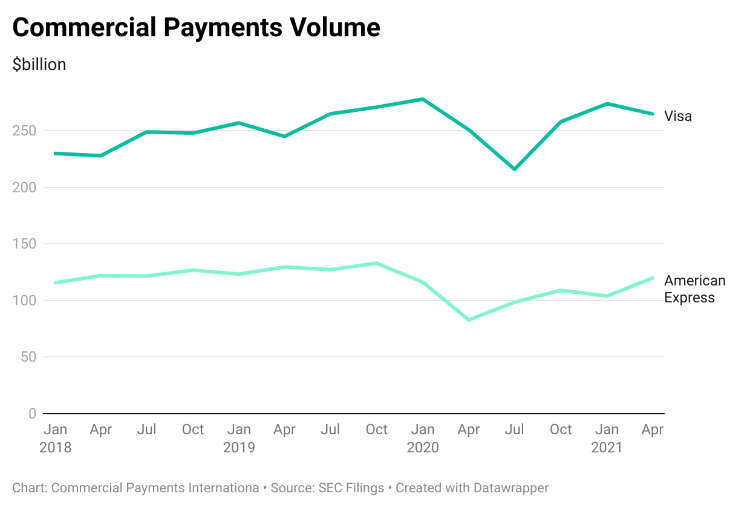

Since the start of the pandemic, the global card giants – Mastercard, Visa and American Express – have consistently shown commercial payments business below pre-pandemic levels.

In the latest SEC filing of Q2 2021, American Express has recorded a rise of 3.3% as compared to Q1 2020 and a notable increase of 44% from Q2 2020 in proprietary billed volume to $119 billion. Its counterpart and arch-rival, Visa has recorded a commercial billed business at $265 billion in the same period which is down by 3.3% from the previous quarter.

American Express’ per commercial card spending also jumped to $8,180 which is 14.2% higher than Q1 2021 and the company recorded a rise of 2% in cards in force to 14.8 million.

In terms of new customer acquisition, American Express CFO Jeff Campbell noted that, “acquisitions of new U.S. consumer and small business platinum and gold cards all reached well above 2019 levels this quarter”.

Mastercard in its Q2 2021 financial results has revealed that its Gross Dollar Value (GDV) has jumped by 38% as compared to Q2 2020 to $1,904 billion and by 11% from Q1 2021. It also saw an increase in cross-border volume fees where it grew by 69% from Q2 2020 to $1,076 million and by 15% from Q1 2021. Unlike its competitors, Mastercard doesn’t break out commercial cards volume separately.

The company’s CFO, Sachin Mehra, in a Q2 2021 earnings call noted that the path to recovery in B2B payments remains uncertain due to new variants in Covid-19 and progress of vaccination and “therefore, the pace of recovery may not be linear”.

American Express in its quarterly presentation noted that under global commercial billed business growth, Small and Medium Enterprises have shown a 44% YoY growth and 6% growth as compared to Q2 2019, putting them at pre-pandemic levels. While for Large & Global Corporates, the growth remains 34% up YoY and down by 51% compared to Q2 2019.

AmEx’s CFO, Jeff Campbell, noted in the company’s earnings call that, “large and global corporate card spending, which historically has been primarily for travel and entertainment, continued to show fewer signs of recovery. We have said all along that we expect this will be the last customer type to see travel recover”.

As in the arena of Travel and Expense (T&E) segment, American Express disclosed that the SMEs T&E segment was down by 42% compared to Q2 2019 but 298% up from Q2 2020 and in the case of large & global corporates, it was down by 82% and up by 189% in the same period. The company said its T&E segment had reached 70% of 2019 levels in the second quarter of 2021 and the company assumed “that overall T&E spending globally will have recovered to around 80% of 2019 levels by the fourth quarter of 2021”.

But taking particularly on the corporate travel segment, the company’s chairman and CEO, Steve Squeri said, “we’re not assuming very much from a corporate travel perspective, minimal improvement from really where we are”.

Echoing this, Visa’s Vice Chairman and CFO, Vasant Prabhu, also noted that the company has seen ‘higher cross-border volumes from a faster-than-anticipated recovery in travel’ and that ‘travel is approaching 2019 levels in July’.

In Q2 2021, American Express Global Business Travel (GBT) had announced the acquisition of Egencia which was part of Expedia Group’s corporate travel arm and Visa signed a partnership with TripActions for an expense management solution in the travel industry.

On the contrary, Mastercard continued its expansion in the Middle-East and Africa region, this time it signed a partnership with Penny Software to launch Mastercard Track Business Payment Service.

Talking about the Mastercard Track Business Payment Service, the company’s CEO, Michael Miebach, noted that the company is making ‘progress with Mastercard Track building out our global open-loop network by working with buyer agents and supplier agents such as banks, software companies and ERP vendors’.

Additionally the company’s CEO in the Q2 2020 earnings call emphasized the fact that B2B is a TAM (Total Addressable Market) of $125 trillion and the company would take a step ‘one bit at a time’ and the initial focus on the commercial business side would be on small businesses and virtual cards.

“I think this continued interest in digitizing B2B supply chains and B2B payments, that will also play out and grow overtime over the next two, three years”, said Michael Miebach.

In the last quarter, the company announced that it has partnered with Eedenbull to improve its Commercial Payments as-a-service (CPaaS) solution while it also teamed up with Barclaycard Payments to provide its Track Payment Service.

It also established a real-time payments gateway in the UK which the company says will provide flexible access into the UK’s real-time payments infrastructure for Financial Institutions and Payment Service Providers.

Its rival, Visa partnered with Goldman Sachs for cross-border payments and with Airwallex it launched a B2B payments card for business clients in the Asia region. After a failed acquisition of Plaid by Visa, the company in Q2 acquired Tink for €1.8 billion and signed an agreement to acquire Currencycloud at a valuation of £700 million.