Commercial payments giants continue to bleed amid pandemic

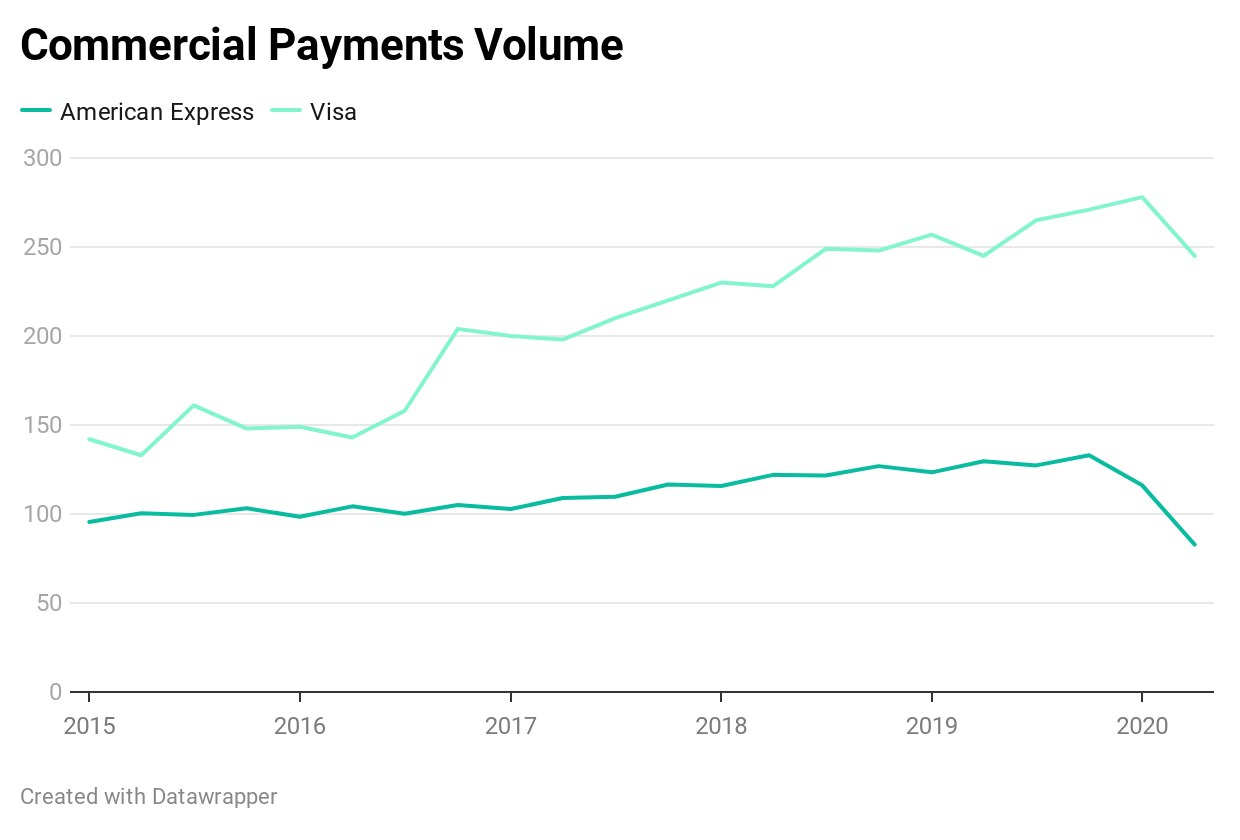

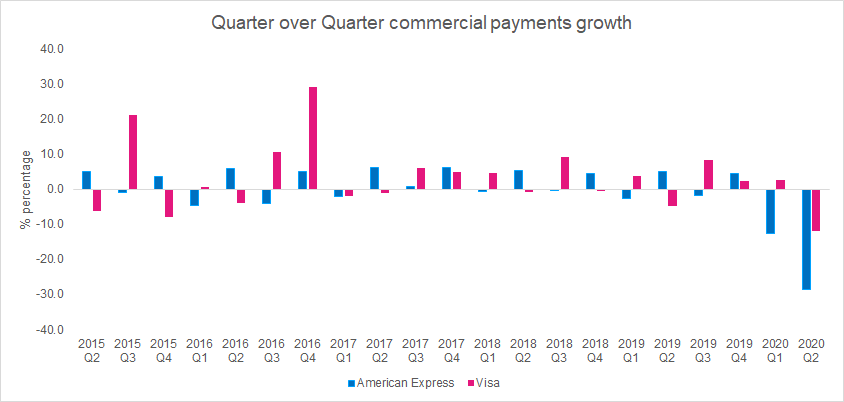

American Express recorded a 28% decline in commercial payments volume in Q2 2020 while Visa fell by 12%. The travel and expense category continues to be the hardest hit.

After warning about the Covid-19 impact on their commercial payments business earlier in the year, card giants Mastercard, Visa and American Express have reported another dismal quarter’s results. In Q2 2020, the severity of the downturn markedly increased compared to their Q1 results, suggesting that it is far from over.

In its latest SEC filings, American Express recorded $82.8 billion in commercial payments business. This was down from $116 billion in Q1, representing a 28% decline. It is the company’s single largest fall in commercial payments volume, as is the second straight quarter over quarter decline. Rival card firm Visa Inc. reported a 12% decline in commercial payments volume, falling to $245 billion from $278 billion in the previous quarter.

Commenting on the Covid-19 situation on a Q2 investors call, CEO of American Express Steve Squeri said, “there is still much uncertainty about the economic environment as reopenings are stalled in a number of geographies and status of government support programs remains unclear”. Squeri also noted that the company had hit the “trough” in mid-April for Q2 spending.

T&E spend particularly feeling the pinch

Mastercard does not disclose its commercial payments volume figures in its 10-Q SEC filings. However, the firm’s president, Michael Miebach, said on its Q2 2020 earnings call that “the COVID-19 pandemic has triggered a series of significant behavioural changes across consumers, merchants and businesses to having a profound impact on payment preferences”. According to the company, Gross Dollar Value (GDV), which includes consumer and commercial spend, declined by 12% from $1565 billion in Q1 to $1383 billion in Q2. The most prominent effect was seen in Mastercard’s cross-border payments revenues which dropped from $1.21 billion in Q1 to $647 million in Q2, a 47% decline QoQ.

Miebach did provide a note of optimism for the revival of T&E spend, however, as he noted in investors call that “once border restrictions are lifted, we will see some increase there”.

All three commercial payments giants have reported the fall in T&E spend. Mastercard observed that the decline in cross-border spend was due to border restrictions, while Visa noted in its investors call that travel category was 50% down in the April-June quarter. American Express reported a 100% to 75% decline in T&E from the April-June quarter.

Last month, Commercial Payments International hosted a webinar on Travel and Expense activity wherein the panel observed that the recovery in this segment will not be seen until 2023. However, in the same period, overall B2B payments will soar to $785 billion in 2023 from $496 billion in 2019, MD Commercial Payments at Accenture, Frank Martien said during the webinar.

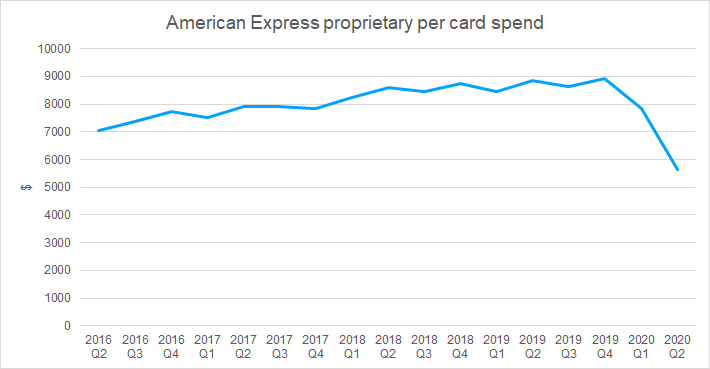

In Q2, American Express saw the sharpest decline in average card per for its proprietary business where it dropped by 28% to $5,465 per card.

Slowdown can’t halt commercial payment investments

Despite the drop off of commercial payment flows in Q2, the big three commercial card firms continued to expand their B2B payments footprints with new acquisitions, partnerships and product launches.

American Express launched its accounts payable solution for US businesses. The company also formed a joint venture with Express (Hangzhou) Technology Services Company Limited that received approval from People’s Bank of China (PBOC) for a network clearing license, allowing it to become the first foreign payments network to be licensed to clear RMB transactions in mainland China.

Also in the past quarter, Mastercard announced Mastercard Track Business Payment Service that aims to expand and modernise B2B payments in the US. It also had a Chinese project, partnering with Bank of Shanghai to support international businesses sending money to China. The company also launched its fintech program in Europe, in which Railsbank become the early adopter, followed by Treezor. EedenBull partnered with Mastercard in fintech space in Europe and Asia-Pacific region, and Tide became the principal issuer after its partnership with Mastercard for UK’s SMEs.

Visa funded cross-border payments platform Nium in Q2, and the two also later collaborated to expand card issuance services into Europe and Australia. In the fintech space, Soft Space and BPC joined Visa’s Fintech Fast Track programme.